"Financial sponsors have been relatively quiet the last two years, with most of them focused on raising new capital, returning capital to LPs, or a combination of both. We are starting to see that dynamic change with more constructive markets."

Vivek Bantwal, Head of Global Financing Group

As the markets continue to heal and sentiment improves, we expect 2024 to be a year of rebalancing, bolstered by renewed optimism, fresh pools of capital and pent-up demand. A recalibration of markets and alignment of valuations have given way to a unique set of opportunities.

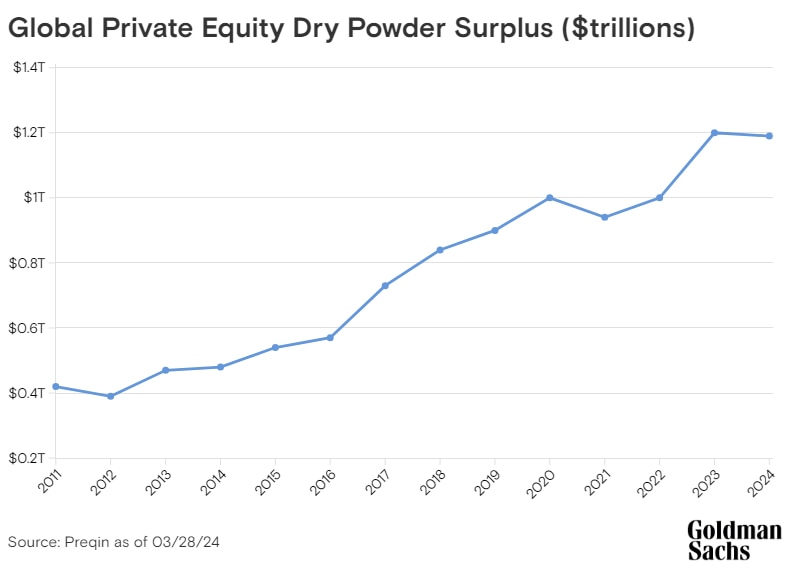

A key driver? The growth and diversification of alternatives, which continue to rapidly accelerate. The growing dry powder surplus — amid expectations of central bank cutting cycles around the globe — is fueling momentum that has already begun to bolster M&A volumes (Q1 activity was up 34% YoY) and financing markets, as an overall reopening takes hold.

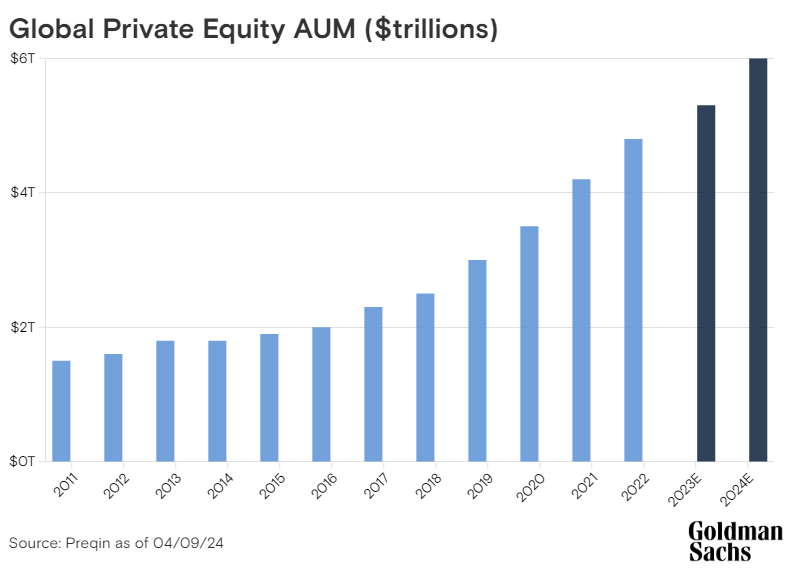

Private Equity Inflection Point explores how macro drivers, coupled with an unprecedented $1.2T in PE dry powder and an estimated $6T in PE assets under management (AUM), have primed the capital markets for what we expect to be a robust ripple effect of strategic and financing opportunities through 2024 and beyond.