Note: The following was published as part of the March 27, 2017 edition of BRIEFINGS. For more insights from Goldman Sachs sent straight to your inbox, subscribe here.

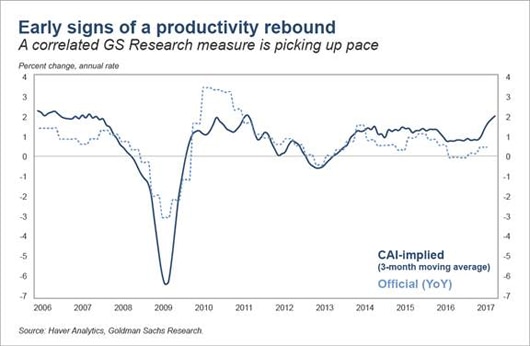

Could there be signs of a turn in the productivity slump that has puzzled economists since the financial crisis? Labor productivity in advanced economies has grown at an average pace of just 0.75% since 2008, down from 2% in the three decades before, a trend that Goldman Sachs Chief Economist Jan Hatzius has termed the "productivity paradox" given the pace of technological advances. The pessimistic story is that this weakness reflects a lasting slowdown in the pace of innovation and capital accumulation. A more optimistic story is that it is due to temporary hangover effects from the financial crisis, increased measurement error in a more rapidly changing economy, or both. Hatzius has argued that measurement error has increased, but it can only account for some of the weakness -- perhaps 0.25-0.50 percentage points of deceleration in the United States, and probably less elsewhere. Thus, the key question is the importance of any temporary hangover effects. He and his team in Goldman Sachs Research see two reasons why temporary hangover effects may have been important. First, a decomposition of productivity into its underlying drivers shows that slower growth in capital services per hour worked has been the most important drag. This looks like a cyclical consequence of the weakness of capital spending since the financial crisis, and there are some early signs that this weakness is abating. Second, while the official productivity data remain lackluster, they are quite lagged and there are some early signs of improvement in the higher-frequency indicators. A decomposition of GS Research's Current Activity Indicator (CAI) shows that output-related indicators have been growing more rapidly relative to employment-type indicators over the past year or so. Historically this has been associated with acceleration in the official productivity measures over time.

The data provided in this newsletter is for information purposes only and should not be construed as investment or tax advice nor as a recommendation to buy, sell, or hold any particular security. Goldman Sachs believes the data in this newsletter is accurate, but does not verify its accuracy independently and does not warrant or guarantee that it is accurate or complete. Goldman Sachs has no obligation to provide any updates or changes to the data. No investment decisions should be made using this data.

To the extent this newsletter includes material from the Goldman Sachs Securities Division, please click here for information relating to Securities Division material and your reliance on it.