Retail Investors Are Sticking with the US Stock Market—So Far

The S&P 500 Index this year has fallen by the most in decades, as investors reckon with everything from lockdowns in China to a Federal Reserve that aims to cool the most overheated job market in postwar U.S. history.

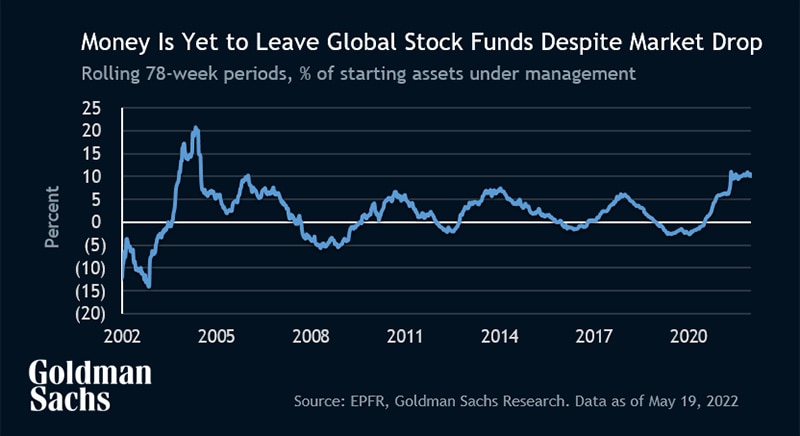

But retail investors, who have become a key force in U.S. equities, have for the most part kept their cool, according to Scott Rubner, a managing director in the Global Markets Division at Goldman Sachs. For every $100 that’s gone into stock funds during the past 74 weeks, only $2 has flowed out. That’s the opposite of professional investors, he says, most of whom have already exited the market.

Money moved out of just about every type of fund last week, including those that invest in stocks, bonds, gold and money markets; technology-stock funds had the largest redemptions of the year. We spoke with Rubner, an expert on fund flows who is on the derivatives sales and macro execution team in New York, about whether the COVID-era flood of money into these funds is starting to reverse, and what that means for the S&P 500 Index of U.S. stocks and other assets.

You recently wrote in a note to clients that, for every $100 put in stock-market mutual funds and exchange-traded funds over this cycle, only $2 has been redeemed. Is that retail investing or a mix of institutional and households?

Most people who are trading these products are retail. That jibes with the concept that retail and households are the largest owner of the equity market.

What is your takeaway from these numbers?

The general view is that the largest pool of capital gets panicky when the market reaches its lows. But what this is saying is that there’s a lot of money that’s flocked into the equity market and it’s not come out. I don’t expect it to come out.

I only expect it to come out if the market were to materially move lower from current levels, and I view that as down 10%. A way to calculate that is by looking at the average level for the S&P 500 when this investment was flowing in, and then calculate a 10% drop from that average. And down 10% from the average in S&P-equivalent terms is about 3,800. The market is up materially from that level, at about 4,088.

Who could sell from here? The only person who hasn’t sold is households. Everybody else on the professional investor side has sold, is short or has no more to sell. And if retail doesn’t sell from here — because the market has held in at some of the key levels — I don’t see the market crashing.

Some of the measures of liquidity that you look at have never been worse. How much is that contributing to the selloff and what’s going on under the surface?

The drop in liquidity exacerbates the selloff. And liquidity has declined in part because the people who provide liquidity have drastically changed. Now it’s a more quantitative liquidity provider who is very fast and sophisticated — they giveth and they taketh away quickly and suddenly.

At the same time, Goldman Sachs’ Financial Conditions Index has substantially tightened, and the Fed is withdrawing liquidity hand over fist at this juncture.

People were used to buying in a market that went up every single day for the COVID era, and a lot of those traders are new to the equity market. If you withdraw liquidity and start seeing redemptions, you could open up some downside on, specifically, some non-profitable tech companies.

You pointed out to clients that for every $1 invested in the SPDR S&P 500 ETF, 22 cents of that is concentrated in the five biggest companies in the fund. For Invesco’s QQQ ETF that tracks the Nasdaq 100 Index, 42 cents of every $1 dollar is concentrated in the five biggest stocks. What is your takeaway from those figures?

The market has had a robust period of inflows over 74 weeks. That money mostly went into U.S. products — S&P 500 and Nasdaq. And by buying passive ETFs you are buying those top five stocks — the big tech companies. That by definition is the largest and most-owned place that investors had been hiding. And that is also the world’s 401(k) portfolio.

These things basically went a year and a half without redemptions. But now redemptions are starting to pick up. You’ll know that retail stock investors are starting to capitulate when those big tech companies tumble in price.

Is there more trading in ETFs than in single stocks? Does that matter?

Last week on one particularly volatile day, ETFs represented 45% of the overall tape in the U.S. This is not normal. To me, that suggests that it is macro and long-short hedge funds and professional investors hedging around liquid macro products and not trading the underlying.

If you get tapped on the should by your risk manager and they say, “hey, you need to reduce the portfolio,” then the way you do that is you walk in and you short futures and you short the big ETFs. That isn’t fundamental investing — that’s risk management and it’s not sustainable. We’ve never seen stats like that.

For the market structure to heal, it needs for ETFs to be a lower percentage of volume and more fundamental trading where we can get true price discovery.

To the extent this publication includes material from the Goldman Sachs Global Markets Division, please click here for information relating to Global Markets Division material and your reliance on it.