Outlook 2022: The Long Road to Higher Rates

- GS Macro Outlook 2022: The Long Road to Higher Rates08 November 2021

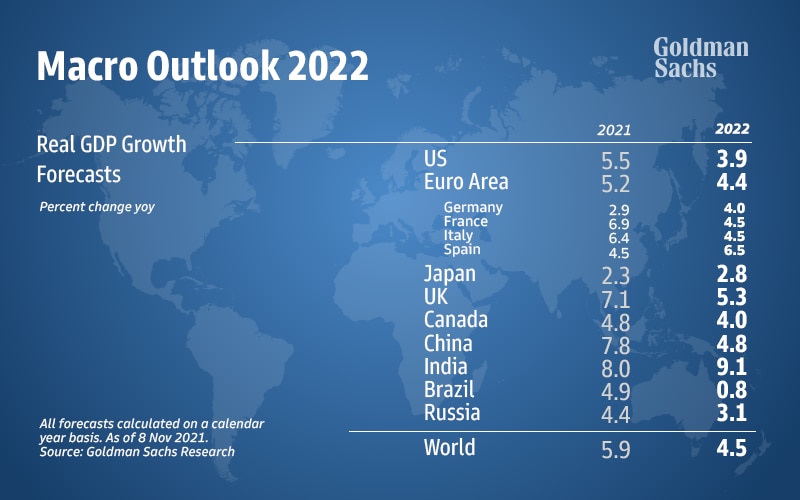

Although the fastest pace of recovery now lies behind us, we expect strong global growth in coming quarters, thanks to continued medical improvements, a consumption boost from pent-up saving, and inventory rebuilding. For 2022 as a whole, global GDP is likely to rise 4½%, more than 1pp above potential.

The major DM economies should grow rapidly through midyear and then moderate gradually as the near-term impulses wane. In EM, we expect comparatively sluggish performance in China, where the property market is likely to soften further and macro policy looks set to ease only modestly, and in Brazil, where financial conditions have tightened sharply and a potentially messy election looms. By contrast, we are more optimistic on India because of significant catch-up potential and on Russia because of a boost from the oil and gas sector.

The biggest surprise of 2021 has been the goods-led inflation surge. This recently prompted us to pull forward our forecast for Fed liftoff by a full year to July 2022. Subsequently, we expect a funds rate hike every six months, a relatively gradual pace that assumes a normalization in goods prices and in overall inflation (albeit later and more partial than we previously thought).

By the time Fed hikes get underway, some advanced economies (including the UK and Canada) should be well into the interest rate normalization process, and a number of economies in Latin America and Eastern Europe may already be approaching its end. By contrast, we think the ECB and RBA are still far away from hiking rates, and markets seem to have overshot in their expectation of an imminent hawkish turn.

Beyond the next few years, we expect nominal policy rates across most DM economies to rise well beyond the rock-bottom levels now priced in the bond market. For one thing, inflation should settle ½pp above the pre-pandemic level on average, in part because central banks have tweaked their goals accordingly. Moreover, neutral real rates are more likely to rise than to fall, given increased political tolerance for budget deficits and climate-related investment needs.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

By submitting this information, you agree that the information you are providing is subject to Goldman Sachs’ Privacy Policy and Terms of Use. You consent to receive our newsletter via email.