Europe’s Path to a Sustainable, Reliable, and Affordable Energy Future

Among the senior leaders interviewed (L-R): Gonzalo Garcia, Michele Della Vigna, Philippe Camu, Letitia Webster

Russia’s invasion of Ukraine has upended the European energy playbook. To better understand the current situation and future possibilities for the continent’s energy needs, we asked senior leaders throughout Goldman Sachs for their analysis.

Gonzalo Garcia, Co-Head, Investment Banking, EMEA: “The “weaponization” of energy by Russia in its war against Ukraine has brought to the forefront Europe’s critical, decades-long dependence on abundant, stable, and cheap energy. Arguably, cheap energy supply was one of the pillars that supported the industrialization of Europe in the 20th century. European industry and consumers were the most logical market for Russia’s abundant gas reserves: It was and still is the cheapest source of energy available for Europe.”

Russia’s invasion of Ukraine has compounded years of under-investment in global energy supply and distribution.

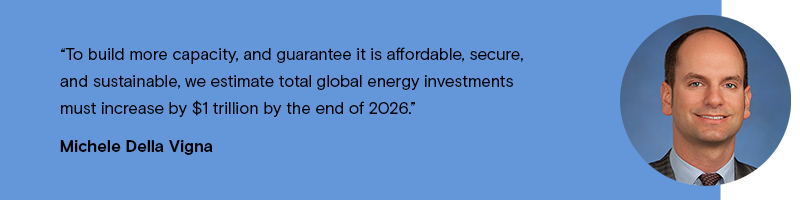

Michele Della Vigna, Head of Carbonomics and EMEA Natural Resources Research: “Investments in what we call traditional energy (oil and gas) fell 57% from 2014 to 2020. Moreover, total energy investments fell 22%. That means not only was there an abrupt drop in the traditional energy space, but investments in renewables, which are currently smaller in scale and require higher capital intensity, didn’t keep pace.”

The combination of a geopolitical shock and under-investment has created an affordability in crisis not just in Europe, but globally.

Michele Della Vigna: “In Europe, we estimate the direct energy cost to the average consumer has increased by 50% per capita on average this year, to the highest level in decades. In the United States, the average direct energy cost per capita has also reached the highest level in two decades.”

Adapting to the new status quo can accelerate the transition to more reliable and sustainable energy sources, but that transition still requires considerable time and money.

Valentijn van Nieuwenhuijzen, Global Head of Sustainability, Asset Management: “In my view, this energy crisis has created a stronger price incentive than any policy, regulatory, or tax incentive. We already see spiking demand for solar panels, massive house improvement focused on insulation, and green capex by corporations. However, gas dependency remains very high. The needed investment in infrastructure is massive and will take time to be implemented. The incentives for change are there; the time to execute remains a bottleneck for the speed of transformation.”

Clemens Tripp, Sustainable Banking Group, Investment Banking: “What makes this challenging is that the transition requires significantly increased spare capacity than in the current energy system, due to the intermittent nature of renewable power. That means there needs to be a focus on power storage, vastly improved grid networks, and incentives to maintain spare capacity for periods of strong demand or where renewables face supply issues.”

While Europe has been reluctant to base an energy strategy on liquid natural gas (LNG), the fuel will remain a key part of its supply in the years ahead.

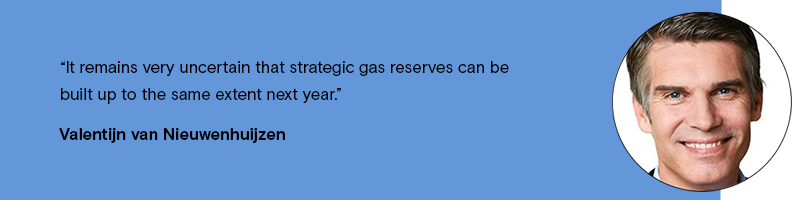

Samantha Dart, Senior Energy Strategist, Commodities, Research: “Our view is that Europe can get through this winter without blackouts because of how much LNG storage was built. The problem is we get to spring, and we must do it all over again… The only sustainable solution to this problem is for Europe to get its hands on additional supplies of natural gas. The problem is that projects being built to supply more natural gas are only set to come online in 2025 and 2026, so it's going to be a couple more years of big challenges for Europe.”

And Europe could be challenged further: Everything from the weather forecast to the Chinese economy could affect global LNG supply.

Samantha Dart: “Natural gas is a very seasonal commodity, so a colder turn of the weather can significantly affect both balances and prices. The main risk ahead is Chinese demand. China was the largest buyer of LNG last year, but this year, because its economic growth slowed significantly, its purchases slowed, leaving a lot more supply available for Europe. If China rebounds into next year, it's going to buy more LNG. It's something that we already expect, but the extent to which it's going to play out is absolutely an important source of risk as well.”

Moving away from historic sources of energy will have a significant impact on Europe’s energy economy, with ramifications well beyond the cost of any given kilowatt.

Gonzalo Garcia: “If Europe is determined to cut its dependence from Russian gas, one thing is for sure: energy will be significantly more expensive in Europe.”

Clemens Tripp: “The long-term competitiveness of certain sectors in Europe—especially those which need gas as feedstock, as well as industrial sectors requiring significant amounts of power, is under serious threat. We are seeing gas demand destruction in Europe, with consumption in the second quarter of 2022 down 16% year over year, driven by the chemicals and fertilizer sectors.”

Those companies that have already made significant changes in their energy strategy are feeling the benefit.

John Goldstein, Head of the Sustainable Finance Group: “The relative performance of companies that have already achieved significant energy efficiencies in their operations and supply chains against the backdrop of the energy crisis is a reminder of the fact that, independent of any market perspectives on ESG and sustainability, efficient use of physical capital is a powerful lever for protecting margins and enhancing resilience.”

With the cost to hedge soaring this year across commodities, support for financial markets will be crucial, in both the short and longer term.

Clemens Tripp: “With the increase in commodity prices, collateral requirements have significantly increased for market participants (corporations, traders, financial players), tying up liquidity and credit capacity, and in some cases preventing market participants from incurring hedge positions given lack of available credit lines, raising questions around the functioning of these markets. As seen in the European utilities space, governments could consider providing credit support to market participants to enable energy supply and hedging activity, and also promote investment activity by helping secure future returns.”

Managing the transition effectively will require participation from governments, corporations, and investors among many others, each with their own role to play.

Philippe Camu, Chairman and Co-Chief Investment Officer of Infrastructure, Asset Management: “Private investors and corporations can aim to provide both the capital and the expertise required to build the infrastructure to reach net zero. That infrastructure includes investments for the generation, the transmission, and the storage of green power as well as investments to enable the transition from domestic and commercial combustion engines to EVs. To accelerate and facilitate those private investments, I believe that governments should establish the frameworks that offer the visibility and the stability that are essential for infrastructure investors. Particularly around regulation, planning process and connection to the grid.”

Kara Mangone, Global Head of Climate Strategy: “Collaboration is critical. Alongside our clients and policy makers, development banks and non-profits can all help to address gaps we see in the market.”

Legislation is already helping to catalyze the move to sustainable fuels: The EU’s REPowerEU plan lessens dependence on Russian LNG in favor of renewables; the U.S. Inflation Reduction Act incentivizes green-energy efforts at a crucial time.

Kara Mangone: “The IRA will transform the economics around essential decarbonization technologies like green hydrogen and carbon capture and incentivize both corporate and individual consumers to make purchases that improve the energy efficiency of their property and transport.”

John Goldstein: “The clarity, significance, and duration of support for key technologies, from renewable generation, to energy storage, to carbon capture, combined with robust and growing demand is a potent cocktail.”

But while the U.S.’s IRA is increasingly seen as the new benchmark, tensions with trade partners notwithstanding, European regulatory models can and should be used to encourage private capital deployment:

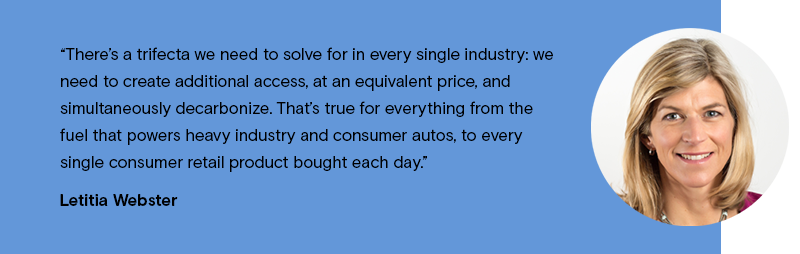

Letitia Webster, Head of Sustainability for Private Investing, Asset Management: “As much as legislation is designed to institutionalize standards and mitigate risk, policy should also seek to center the solution providers and level up the support for innovation so that the playing field is more even versus traditional energy sources. With that in hand, private markets can then step in and really fund the change we need at serious scale.”

Gonzalo Garcia: “Europe was a pioneer in creating regulatory models that give investors visibility over the financial returns they can expect from their investments in public projects. I would argue this is essential to encourage private sector investment in infrastructure where the capex deployment is front loaded and the returns accrue over a long period of time, often several decades.”

Investors are increasingly requiring corporations to take climate into account when planning future strategies, but those requirements are not being applied evenly.

Michele Della Vigna: “Investor pressure shows a clear bias toward energy producers versus energy consumers, with data since 2014 showing more than 50% of proposals targeting energy producers (oil & gas, utilities), while only 30% of the proposals target sectors that account for most of the final energy consumption.”

Continued government support for households is already proving crucial in the aftermath of Russia’s invasion of Ukraine, but the larger burden the energy transition could place on lower- and middle-income consumers around the world needs to stay front of mind.

Jari Stehn, Chief Europe Economist, Research: “There’s a high degree of heterogeneity even within Europe as nations direct consumer support and subsidies. Most measures and support have been aimed at households, through retail price caps, gas and electricity. We’ve also seen rebates for petrol. That support for households as we move into the winter months is an important reason why we think the recession is going to be more limited, especially in terms of depth.”

Valentijn van Nieuwenhuijzen: “A critical condition to make this transition "just" must be a household income policy that uses proceeds of pollution pricing and taxes to compensate the impact on disposable incomes.”

Kara Mangone: “While the situation in Europe is in focus, climate disasters and access disasters persist globally, with devastating results. We believe policy and energy spend can bend this trajectory over time.”