Markets

Are US Stock Market Valuations Outpacing Fundamentals?

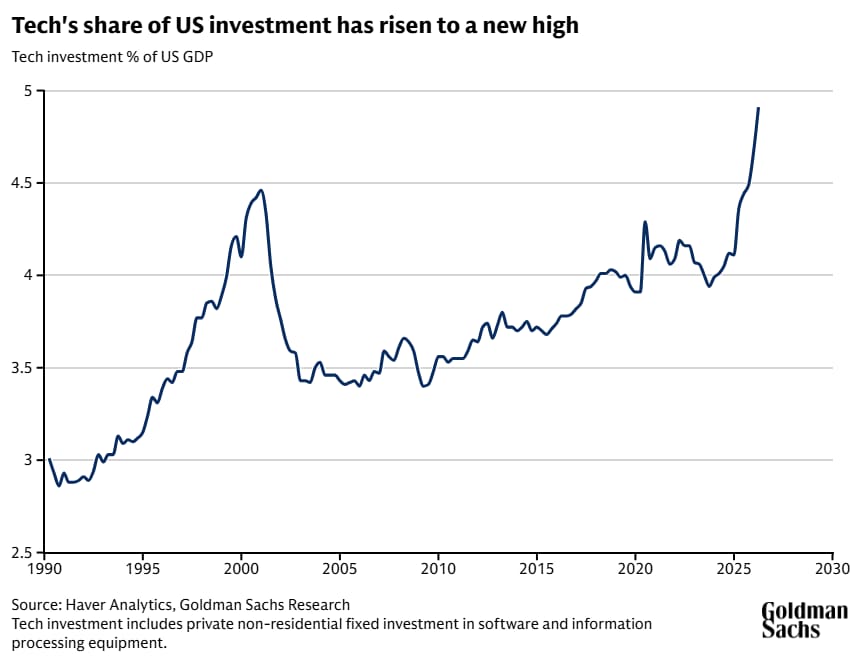

- US tech investment as a share of GDP has surpassed its 1990s peak, and spending plans from the largest cloud and computing companies for 2026 are nearly 50% higher than estimates from just six months ago, according to Goldman Sachs Research.

- Unlike the dotcom era in the late 1990s, corporate profits have risen to new highs rather than deteriorating, the current account deficit has narrowed, and corporate balance sheets have remained stable.

- AI-related companies have added roughly $27 trillion in market value since late 2022. It is still possible to reconcile this market value with a macro estimate of future profit gains, but doing so requires more optimistic assumptions.

- The most plausible upside stories rely on AI-related companies capturing a higher share of the economic gains from AI than normal. But there is a risk that investors may be overestimating how long above-average profits will last, particularly for companies supplying AI infrastructure.

The boom in artificial intelligence (AI) investment has entered a more intense phase, but the broader economy has not followed the same script as the wave of technology investment during the dotcom era, according to Goldman Sachs Research.

Four key macroeconomic developments signaled a potential bubble in the late 1990s, Dominic Wilson, a senior advisor in the Global Markets Research Group, and Vickie Chang, an analyst in Goldman Sachs Research, write in a report:

- Sustained investment at unusually high levels

- A decline in profit margins

- A sharp rise in corporate financing needs and leverage

- A widening current account deficit

As of late 2025, those dynamics were largely absent in the AI boom, and only one of them has meaningfully changed since then: The investment boom has accelerated significantly over the past six months.

US tech investment as a percentage of GDP has breached the 1990s highs and has risen more sharply than it did then, Wilson and Chang write. Spending plans from the largest cloud and computing companies for 2026 are nearly 50% higher than they were roughly six months ago.

“The AI investment boom is neither as broad-based nor as long-lived as the 1990s tech boom yet, but it is matching its scale,” Wilson and Chang write.

Why the AI boom is different from the dotcom bubble

Other dynamics are not yet following the 1990s path, according to Goldman Sachs Research. Most importantly, corporate profit margins have climbed rather than eroded.

Wage growth and unit labor costs are rising more slowly than they did in the late 1990s. The corporate sector's finances have held steady because rising profits have largely kept pace with rising investment, Goldman Sachs Research finds. International imbalances have not increased—the US current account deficit has been shrinking instead of growing.

Can market gains in AI stocks be squared with the macro outlook?

AI-related stocks have had impressive gains over the past few months. However, a key difference relative to the end of the 1990s boom is that earnings, and earnings expectations, have also been rising rapidly, Wilson and Chang note.

Conventional valuations of the US equity market are high by historical standards. But with earnings expectations rising, forward-looking price-to-earnings measures have not risen this year, even with the ongoing rally in stock prices. Market gains have been more “earnings-driven” than “valuation-driven” lately, according to Goldman Sachs Research.

At the same time, Goldman Sachs Research has estimated the value of the potential additional profits that could be created by AI productivity gains. The researchers’ baseline estimate of the present discounted value of potential AI-related capital revenues to US companies comes to roughly $9 trillion. By comparison, AI-related companies have gained approximately $27 trillion in market value since November 2022. Seven months ago, that gain stood at about $19 trillion.

Those figures can change significantly depending on the underlying assumptions. Wilson and Chang point out that not all of the $27 trillion gain in market value is attributable to AI alone. Many companies (the hyperscalers in particular) have substantial non-AI businesses that may have driven gains in their stocks over that same period.

In addition, more optimistic assumptions about revenue shares, adoption speed, and productivity gains can raise the estimated value derived from AI. But closing the gap between the rise in market valuations and Goldman Sachs Research’s estimates "needs increasingly optimistic assumptions," Wilson and Chang write.

The most credible stories for substantial stock gains depend on the assumption that AI companies earn a bigger slice of total profits than the average company in Goldman Sachs Research’s baseline forecast, Wilson and Chang write.

The economy-wide profit share has trended higher for some time and has risen more sharply again recently. High profitability has been a key part of avoiding macro imbalances, limiting the rise in valuations and dampening concerns about credit quality.

Will the increase in AI-related corporate earnings persist?

“The underlying assumption that the market is making is that this process will continue,” Wilson and Chang write. By driving up prices in line with earnings (even without raising valuations), the market is assuming that these shifts in earnings shares are likely to be highly persistent, that companies involved in supplying the boom will capture a large portion of the potential economic gains from AI, and that the share of profits economy-wide will continue to rise.

While there are reasons to think this profit share could rise further still, Goldman Sachs Research points out that competition, investment, and further innovation can erode those gains. “It remains to be seen how solid entry barriers will be in protecting incumbents from subsequent profit erosion,” Wilson and Chang write.

As importantly, the investment boom itself is generating a substantial portion of the profits that justify current stock prices, according to Goldman Sachs Research. When that spending eventually slows, the earnings picture could change significantly.

“The risk here too is that the market is overestimating the persistence of those earnings streams beyond the next 2-3 years, particularly for those who are benefiting directly from supplying the capex boom,” Wilson and Chang write. “Earnings projections a couple of years forward may still look very robust, but it is harder to know what earnings profiles will look like beyond that point after the phase of rapid investment is over.”

Could the AI boom still turn into a dotcom-style bust?

“While comparisons with the late 1990s still look more reassuring than not, we think it is important not to press that point too hard,” Wilson and Chang write. “Analogues can only take us so far. We may simply be discovering that the macro backdrop to this investment boom—and the vulnerabilities that it may generate—is different.”

Outside AI-related sectors, the broader economy looks considerably weaker than it did in the late 1990s. Consumer spending growth has been relatively modest, real disposable income has grown much more slowly, and non-tech investment has been soft. “The AI boom currently may be offsetting a more fragile macro backdrop,” Wilson and Chang write.

Because the path of profits and earnings looks different, it is less obvious than it was in late 1999 and early 2000 that the gains implied by the market exceed what the economy can plausibly deliver, Goldman Sachs Research notes. But while the risk of a pure “valuation bubble” seems lower than in the late 1990s, the risk of an “earnings bubble” may be growing, Wilson and Chang write.

“The tension between a favorable fundamental backdrop and high valuations that we have highlighted for some time continues to sharpen,” they add.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.