Artificial Intelligence

Private Markets Are Expected to Have a Growing Role in Data Center Financing

- The depth and breadth of private market financing will be increasingly important in the AI buildout as hyperscalers are expected to spend $5.3 trillion on AI and data centers by 2030.

- Infrastructure funds raised a record $221 billion last year, and their growth may accelerate, potentially reaching $3 trillion in assets by 2030, according to Goldman Sachs Research.

- Hyperscalers will need financing from across markets, structures, and currencies as they potentially bump up against saturation considerations in liquid credit markets and issuer concentration constraints.

- Infrastructure funds had more than $1.7 trillion in assets and $400 billion of dry powder as of September 2025, and they are fundraising at a faster pace than a few years ago.

The financing needs for artificial intelligence (AI) are enormous, with hyperscalers planning to spend more than $5 trillion by 2030 on technology and data centers. Private market financing will be increasingly important in providing that capital, according to Goldman Sachs Research.

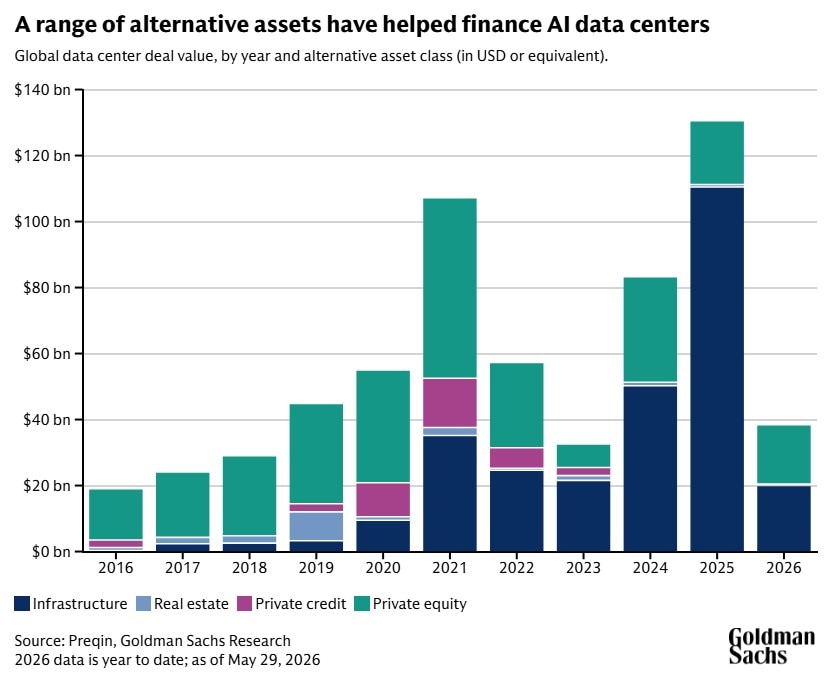

Already, the depth and breadth of the private financing ecosystem have featured heavily in the AI-related investment cycle. “We expect the ‘real assets’ categories of private infrastructure and real estate will play an even larger role in the years ahead,” Amanda Lynam, chief credit strategist in Goldman Sachs Research, writes in a report.

Private infrastructure funds raised a record $221 billion in 2025, and the average fund size jumped to $1.8 billion. The fundraising has been concentrated, with experienced managers capturing the majority of the capital. Infrastructure funds returned 12.8% last year, outperforming all other private market categories except for private equity and venture capital, Lynam writes.

Multiple tailwinds are helping to drive growth for the infrastructure category. From 2021 to 2024, the private infrastructure market grew at a pace of roughly 11.5% per year, based on data from Preqin. Growth could accelerate, according to Goldman Sachs Research, potentially returning close to the 16% to 17% annualized rate that prevailed for much of the decade from 2012 to 2021. If this comes to pass, total private infrastructure fund assets under management (AUM) could exceed $3 trillion by 2030.

How much do hyperscalers plan to spend on data centers?

The scope and scale of planned AI-related capital expenditures have grown immensely. Goldman Sachs Research’s equity analysts expect a combined $5.3 trillion in capital spending from 2025 through 2030 by the large technology companies that are leading the buildout. This tally continues to climb: It stood at $4.5 trillion prior to first-quarter earnings reports.

Lynam’s team has previously highlighted that AI-related financing needs are significant enough that borrowers are tapping options in different markets, ranging from investment-grade debt to private asset markets, across a variety of structures and in different currencies.

Because of their ambitious AI-related capital expenditures, the hyperscalers already account for a large share of new corporate borrowing. They may face market saturation constraints as public debt investors absorb ever-larger amounts of debt from the same handful of issuers (thereby increasing their weights in widely tracked corporate bond indices), or as some investors become less willing to buy the securities because of portfolio concentration limits.

“We expect liquid credit market saturation and issuer concentration constraints to become somewhat more binding in coming years,” Lynam writes. While the magnitude of such constraints is “still heavily debated,” the report says, these issues will at the very least impact nuanced decisions around exposure and pricing, according to Goldman Sachs Research. This is why the ability of the private markets to play a meaningful role in AI-related financing is so important.

How is private capital being used in data center financing?

The lines between private market infrastructure and real estate funds have been blurring. That’s because different aspects of data center financing—including land, operational networks, power, buildings, and equipment—touch different asset classifications. Over the past decade, digital infrastructure funds have increasingly been categorized in the infrastructure group, rather than in real estate.

What matters more than category names, though, is the combined long-term financing capacity across both fund types, Lynam writes.

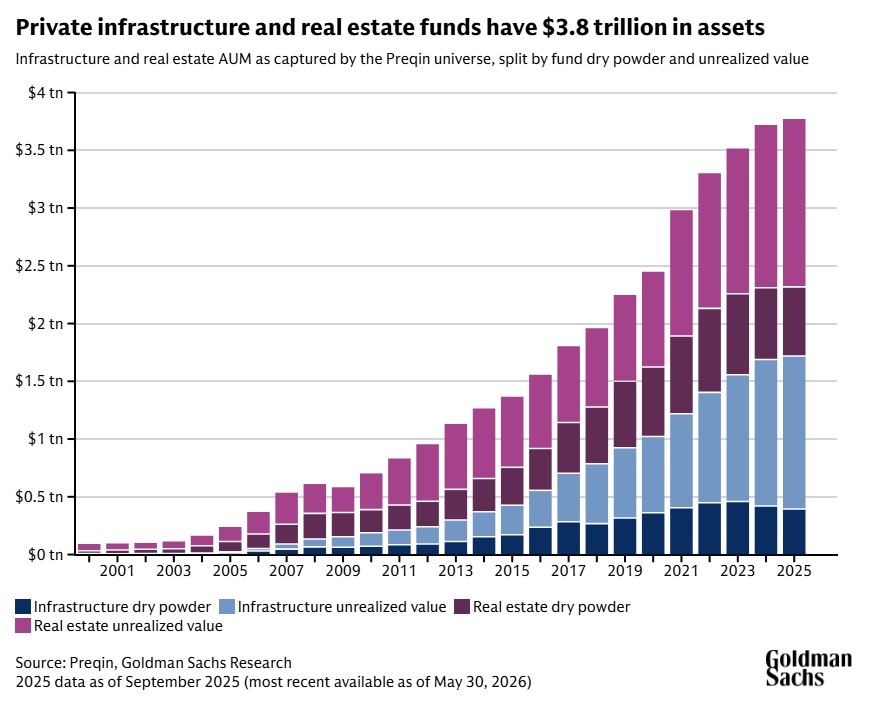

Private infrastructure funds had just over $1.7 trillion in AUM as of September 2025, including almost $400 billion of uninvested dry powder available to be deployed, based on Preqin data. The private real estate market is even larger, with $2.1 trillion AUM, including $600 billion of dry powder.

Why private market infrastructure funds have had strong growth

The tailwinds creating opportunities for growth in infrastructure funds go beyond digital- and energy-related investments for the AI buildout and include investment related to energy security. The top reasons institutional investors cite for allocating to infrastructure funds include their ability to provide diversification, income streams, and inflation protection.

“Infrastructure’s structured income generation stream and inflation protection characteristics (including direct cost pass-throughs, in some instances) are likely to further support growth,” Lynam writes.

Infrastructure funds are not only getting bigger and setting growth records, they are also completing their fundraising more quickly. From 2018 to 2021, the largest infrastructure funds spent 13 to 18 months on average fundraising; from 2022 to the third quarter of last year, the largest funds spent 7 to 12 months on average to reach closing. As of May 2026, there were 695 infrastructure funds in the fundraising phase, targeting an aggregate $555 billion of capital.

As infrastructure funds grow larger, private construction of data centers has accelerated over the past few years, and there’s a significant backlog of data centers not yet in construction. “For now, the growth in hyperscaler capex estimates is meaningfully outpacing the growth in actual data center construction,” Lynam writes. “This metric warrants close monitoring for an estimate on the long-term financing needs.”

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.