Securing and Financing the Future of Water

- Securing and Financing the Future of WaterWater is essential for every aspect of life, yet its pricing, governance, and management often fail to direct flows where they are most needed.

Executive Summary

- Water scarcity is a geopolitical, economic, and technological challenge globally. More than 2.1 billion people globally still lack access to safe potable water. Today, rising demands from agriculture, the technology industry, and power generation are colliding with that lack of access.

- Governance challenges, environmental factors, and market distortions are amplifying the crisis. Water pricing rarely reflects costs, which can discourage investment, drive overconsumption, and obscure infrastructure gaps. Changing weather patterns exacerbate water stresses. And in many countries, outdated legal frameworks further prevent water from flowing to its highest-value uses, while poor management practices compound fiscal pressures on already overstretched governments.

- Water is increasingly an instrument of geopolitical competition. Transboundary water resources are flash points for interstate competition and tension. Non-state actors, cybercriminals, and violent groups in regions like the Sahel exploit water scarcity for strategic leverage. And water infrastructure is at a growing risk of being targeted in armed confrontations, as demonstrated by strikes on desalination facilities during the 2026 Middle East conflict.

- The water economy is increasingly investible. Desalination, wastewater recycling, smart metering, AI-optimized irrigation, and digital water networks are scaling rapidly. Market reforms, including tradable water rights, tiered pricing, revenue decoupling, and cross-border water-for-energy agreements, are beginning to correct long-standing distortions, while public-private partnerships, blended finance structures, and dedicated investment vehicles are mobilizing capital at scale.

- Water infrastructure and innovation present meaningful economic and social opportunities. The convergence of policy reforms, technological maturation, and capital market innovation—ranging from tokenized water rights and infrastructure modernization to environmental impact bonds and microfinance platforms—is laying the foundation for more resilient and financeable water systems globally.

Securing and Financing the Future of Water

Water is essential for every aspect of life, yet its pricing, governance, and management often fail to direct flows where they are most needed. Although water covers 71% of the Earth’s surface, only 3% of the world’s water is fresh.1 Access to that supply is increasingly scarce, contested, and misallocated. Meanwhile, the infrastructure and technologies that determine water availability remain chronically underinvested, leaving a widening gap between supply and demand.

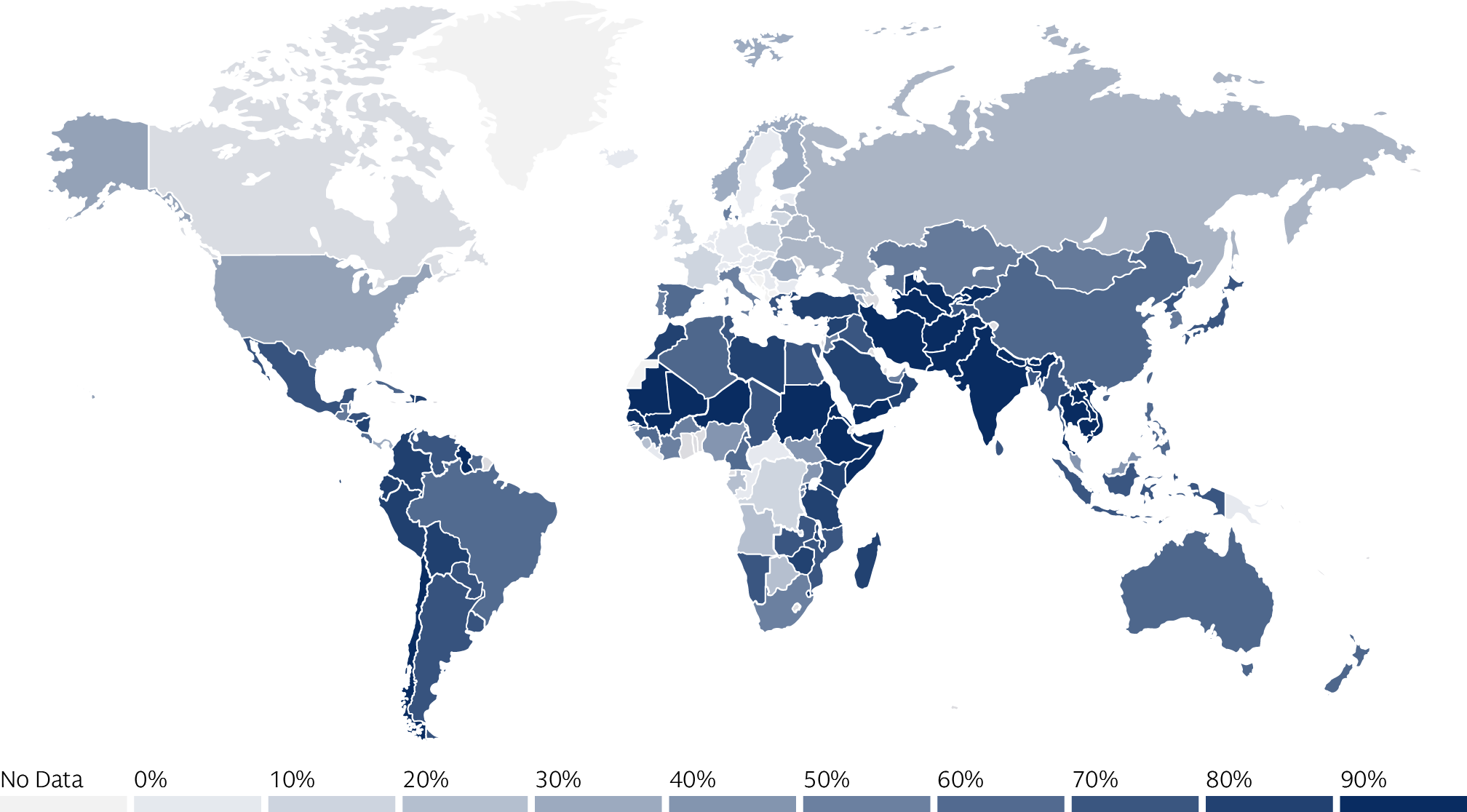

Water demand is rising even as overall supply faces mounting constraints. Despite progress, 2.1 billion people globally2 still lack access to safe, potable water. And water stress—a regionally varying measure of the ratio between demand and sustainably available resources—is increasing. At the same time, water infrastructure is becoming more exposed to geopolitical risk, as seen in recent strikes against desalination facilities in the Middle East. As a result, water is no longer viewed as solely a development-related concern—it is increasingly understood to be a primary strategic issue for businesses, governments, and society.

The market and geopolitical forces shaping the future of water are intersecting with an accelerating pace of innovation. Market approaches are beginning to price water more effectively, more capital is flowing into infrastructure, and new technologies are increasingly attracting investments at scale. These developments remain uneven, but they point toward a more investable and resilient water system capable of laying the foundation for a more sustainable future.

The Economics of Water: Growing Demand Meets a Market Under Strain

Mega-trends are pulling the global water economy in opposite directions. While the commercial water market is experiencing robust growth and technological innovation, the underlying resource base is facing severe shortages, as regional resource scarcity becomes more acute, more widespread, and longer lasting. The World Economic Forum3 estimates that the global need for cumulative total investment through 2040 in water infrastructure is €11.4 trillion, €6.5 trillion more than current investment levels.

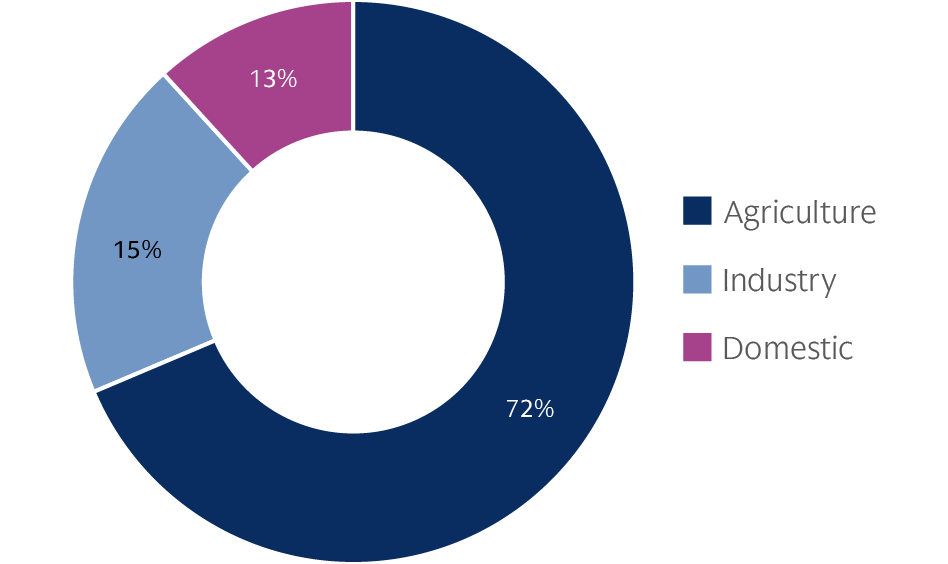

This need is particularly vital for sectors that are politically and socially important, including agriculture, energy, manufacturing, and technology. Agriculture alone accounts for over 70% of global freshwater withdrawals. Meanwhile, the technology industry’s rapid growth is boosting global demand for water. The International Energy Agency4 estimates current global data-center water use at roughly 560 billion liters annually, a figure that could double by 2030, to 1.2 trillion liters. Water also underpins other key physical infrastructure central to technology ecosystems, including electricity-generating assets and semiconductor fabrication plants.

Overflow: Water Market Structures and the Challenges of Governance

Despite their importance, water markets continue to face unresolved tensions between access, affordability, and efficiency. The result is often mispricing and misallocation, limiting or cutting off supply from demand.

Many governments, recognizing water’s centrality, heavily subsidize access. This means that water is often priced below the full costs of treatment and distribution. In the Middle East and North Africa, among the most water-scarce regions in the world, water prices are often around 35% of actual costs.5 Such subsidies serve important social purposes. They can also affect investment incentives, distort allocation, and obscure the challenges of aging infrastructure, leakage, unreliable service, and weather exposure.

Water pricing disputes also often spill across borders. For example, long-standing water arrangements with Malaysia have been central to Singapore’s development, allowing it to import water from Malaysia’s Johor River and sell treated water back at subsidized rates. While the arrangement has secured Singapore’s supply and generated revenue for Malaysia, disagreements over pricing, treaty renewals, and sovereignty have periodically contributed to strains in bilateral relations, prompting ongoing high-level discussions between both governments to find a long-term solution.

Water infrastructure is structurally challenging to finance and capital-intensive, with long time horizons for returns. Large-scale projects, such as desalination plants and wastewater recycling facilities, require significant up-front capital investments and operate over multi-decade time frames.

Additionally, due to concerns about price stability, infrastructure finance is often subject to regulated tariffs that cap returns and limit cost recovery. Across the Middle East, low water tariffs and high subsidies have produced some of the world’s highest per-capita water consumption rates, even as states depend on expensive and energy-intensive infrastructure to meet demand. Financial risk often falls on public budgets, while private investment is stalled and inefficiencies persist.

Challenges to water management can compound these problems. The water pipes supplying Mexico City, one of the world’s largest metropolitan areas, face frequent leaks, sometimes causing as much as 35% water loss.6 In Jordan,7 which copes with chronic water shortages and aquifer depletion, nearly half of its annual water supply is lost to leaks, theft, and inefficiencies. These kinds of losses force governments to spend heavily on water production that never reaches consumers and generates low or no revenue, a fiscal drain that further limits investment.

Outdated legal agreements can exacerbate existing challenges. Legacy water rights and prices disconnected from market realities routinely prevent water from flowing to its highest-value uses at the volumes required. Many of California’s water rights, for example, were established more than a century ago, when the state’s population was less than 10% of what it is now. These rights routinely grant holders priority access even during droughts, reinforced by “use it or lose it” provisions that can penalize conservation. Under this framework, farmers have little incentive to shift away from water-intensive crops, even as the state faces recurring droughts and groundwater depletion.

The rise of the data center economy is adding new pressures on water supply in developed and developing economies alike. Data center cooling and power generation both require substantial water. In the United States, roughly two-thirds8 of data centers constructed or planned since 2022 are located in regions facing severe water stress, which could limit the ability to cool and manage heat produced by AI infrastructure. Data center–related water demand could push some local water systems into deficit by 2030 without major infrastructure upgrades. Similar dynamics may play out in other regions where the AI industry is growing, including in Gulf states, where governments have prioritized AI infrastructure and are building domestic technology industries in some of the most water-stressed environments on Earth.

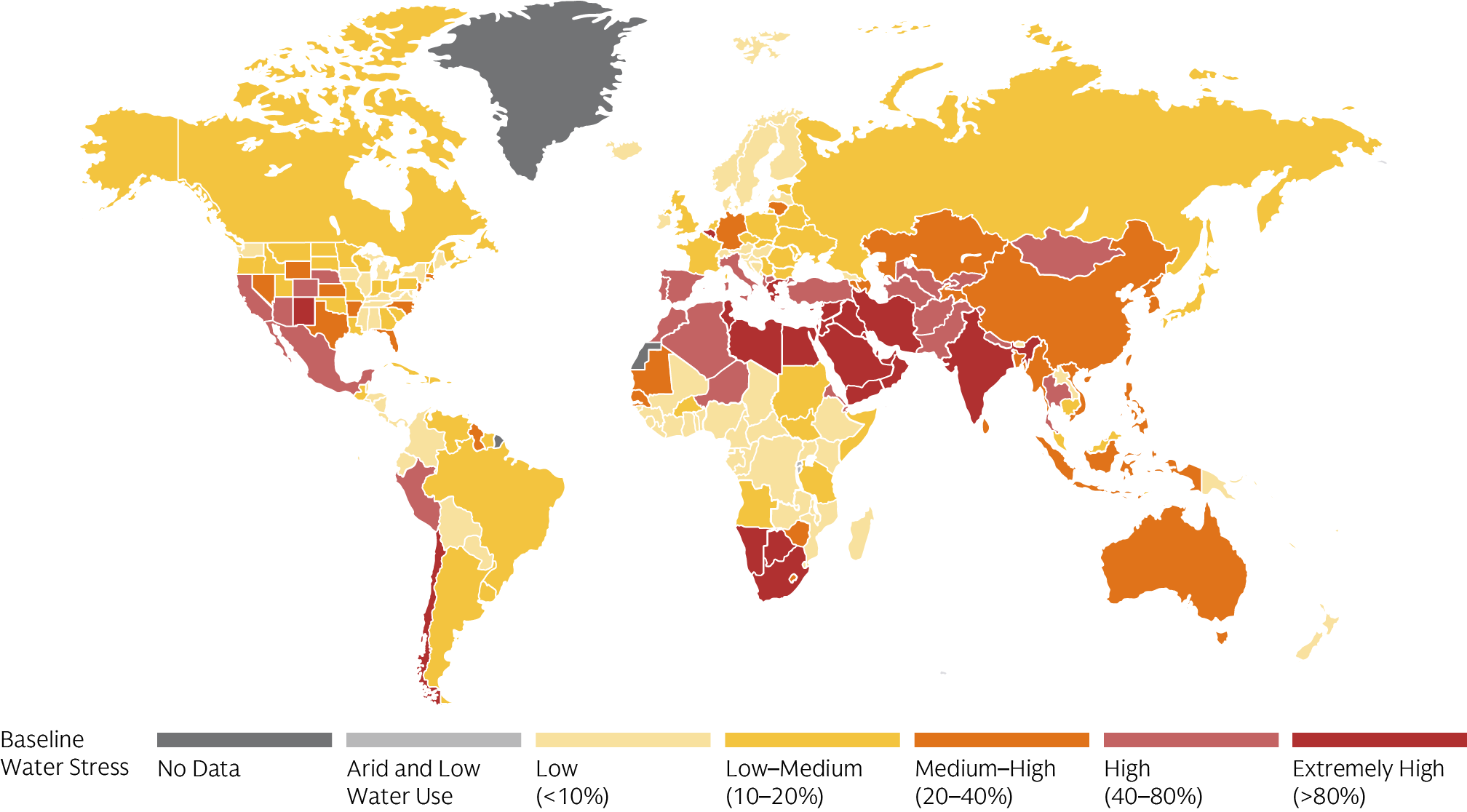

Under Pressure: Natural Reserves and Water Stress

Shifting weather patterns are amplifying water stress, often simultaneously boosting demand, reducing the reliability of supply, and degrading water quality. These pressures are common across the three critical natural reservoirs of the global water system—snowpack and glaciers, surface water, and groundwater—and are often most acute in regions already facing political and economic stresses over access.

Approximately two billion people globally9 rely on mountain snowpacks or glaciers for their water supply. For example, the Tibetan Plateau and surrounding Pamir–Hindu Kush Himalaya mountain ranges and the Hengduan, Tien Shan, and Qilian mountains are home to 100,000 square kilometers of glaciers, originating more than 10 river systems. Warmer weather is increasingly causing glaciers to retreat and regional precipitation to fall as rain rather than snow, which makes it more challenging to retain for future use. Changes in weather are particularly consequential in regions where water systems depend on snowpack, including highly productive agricultural areas like California’s Central Valley, which relies on snowmelt from the nearby Sierra Nevada mountains.

Surface water systems are under growing strain as rising demand, evaporation, and declining quality reduce the reliability of supply. Higher temperatures exacerbate demand and accelerate evaporation of surface water. At the same time, temperature increases cause water quality to deteriorate, with changes in chemical composition and higher concentrations of pollutants and micropollutants limiting usable resources.

Finally, reliable access to groundwater is diminishing in many parts of the world. Groundwater aquifers serve as both a primary source of water and a backstop to variable rain-fed supply, providing roughly 60% of irrigation water globally. However, satellite data10 indicate that global groundwater reserves are declining, with particularly acute stress in some regions, including India, California’s Central Valley, and the Arabian Peninsula. Because many aquifers are transboundary, these declines are also raising the stakes for international coordination—and in some cases, competition—over shared water resources.

The Geopolitics of Water: Scarcity and Statecraft

Water stress is intensifying geopolitical competition. And as many water resources cross international borders, control of flows can be a source of leverage and friction between states.

Water Politics: How Transboundary Flows Shape Power

Water is a long-standing instrument of geopolitical power. At the height of the Cold War, Egypt’s Aswān High Dam became a symbol of the global contest between the United States and the Soviet Union, with regional implications for state power and populations throughout the Nile Basin. China is building a dam across the Yarlung Tsangpo River in Tibet, slated for completion in 2033. Described by Premier Li Qiang as “the project of the century,” the initiative, one of China’s largest ever infrastructure undertakings, has raised concerns among downstream countries about potential impacts on water flows into India and Bangladesh.

Power imbalances heighten existing cross-border tensions. States build dams not only to generate electricity, but also to gain leverage over downstream neighbors. The 1960 Indus Waters Treaty established governance and control over water between upstream India and downstream Pakistan, where more than 80% of agriculture depends on Indus Basin flows. After 65 years, the Indus Waters Treaty was suspended11 in 2025 following a terrorist attack in Kashmir and the brief conflict that followed between Pakistan and India. China’s dam across the Yarlung Tsangpo River has also raised concerns in downstream India, which relies on the river for agriculture, energy, and drinking water, and which worries about the risk that Beijing could leverage water supplies for geopolitical ends. Ethiopia’s Grand Renaissance Dam on the Nile has similarly raised alarm in Egypt, which relies on the river for 90% of its fresh water. These tensions have created a yearslong dispute that remains unresolved, despite mediation by both the African Union and the United States.

Even states that do not share borders can have tensions over water. In Australia,12 nearly 12% of water entitlements are now foreign owned, largely by investors from Canada, the United States, China, and the United Kingdom. In times of scarcity, these legal and commercial arrangements can lead to local pushback against foreign ownership.

Water scarcity also creates vulnerabilities that non-state actors may seek to exploit. Cybercriminals have targeted networks that control physical water systems, heightening cybersecurity concerns for water utilities and related critical infrastructure providers. And in the Sahel, the semiarid region of Africa south of the Sahara, violent groups have used control over water supplies as a means of entrenching their influence from Nigeria to Sudan.

Rivals can target one another’s water infrastructure to inflict pain on civilian populations and coerce competitors and adversaries. During the 1990–1991 Gulf War, Iraqi forces destroyed most of Kuwait’s desalination capacity, with immediate humanitarian consequences. During the 2026 conflict with Iran, Iranian drones struck desalination plants in Bahrain and throughout the Gulf as the fighting in the Middle East expanded to more geographies and targets and the Iranian regime attempted to raise the economic and diplomatic costs of the conflict.

Even prior to the conflict with Iran, the Gulf Cooperation Council member states had zeroed in on water as one of their top economic priorities. Resilience against inefficiency, scarcity, and unexpected shocks were driving factors for this strategy. Attacks on desalination plants and water facilities have not only elevated water as a priority but accelerated the timeline for building increased and more secure capacity.

In many parts of the world, water scarcity has created and exacerbated popular unrest and governance breakdowns within states as well. In 2017, water scarcity in Cape Town, South Africa, became so acute that it was at risk of reaching “Day Zero,” when it would have to shut down drinking water to much of the city. In the years leading up to the Arab Spring, Syria experienced record drought, leading to population displacement. Weeks before protests against the Iranian regime broke out at the end of 2025, President Masoud Pezeshkian stated that the water situation in Tehran was so dire that it might threaten its viability as a capital city.

While water is universally essential, its scarcity and governance challenges resist universal solutions. Treaties such as the UN Watercourses Convention13 articulate principles for shared water bodies—equitable use, avoidance of significant harm, and cooperation on the basis of sovereign equality—to reduce conflict, increase predictability, and guide negotiations. But their impact is limited: Compliance is voluntary, enforcement weak, and participation narrow. Neither the United States nor China is a party to the UN Watercourses Convention or UN Water Convention. Countries have been reticent to join due to concerns about sovereignty and potential impacts on infrastructure development in upstream countries. Despite these challenges, governance reforms continue, marked by the UN’s first water conference in half a century in 2023 and the upcoming 2026 UN Water Conference, cohosted by the UAE and Senegal.

The Future of Water Financing: Market Reforms and Innovation

Water stress is a problem of nature, geopolitics, and economics. But new solutions are coming online. Technological innovations and market reforms are changing how water is managed, priced, and allocated. Novel approaches to sustainable management of land and water resources, together with new technologies and engineering solutions for water collection, distribution, and recycling, provide the technical foundation for water solutions. Governments have a major role to play in helping to scale these innovations, often in partnership with the private sector. For investors and policymakers alike, these developments have the potential to fundamentally reshape the dynamics governing water and to open new market opportunities.

Market Reforms and Public Sector Infrastructure Investments

Market reforms can help mobilize the private sector through direct partnerships and new financing structures and by sending market signals on key technologies like desalination and circularity.

Reforms to water rights and pricing can reduce distortions and better align consumption with scarcity. Allowing holders of water rights to transfer or sell those rights to higher-value uses can improve allocation. Tiered pricing offers another lever with the potential to increase efficiency. In Saratoga Springs, Utah, separate metering for potable water and non-potable irrigation enables adjustable allotments tied to supply, with lower rates for consumption within limits and penalties for overuse. This allows rapid reductions during droughts without altering permanent tariffs or restricting essential services. Revenue decoupling—where utility revenue is separated from volume sold—creates stronger conservation incentives. A 2018 study found that if California’s14 water suppliers had adopted this framework during the state’s 2015–2017 drought, as much as 54.6 billion gallons could have been conserved, enough to supply San Francisco for more than two years.

Updated water arrangements within and between countries can better balance supply and demand across borders and sectors. In Central Asia, agreements allow Kyrgyzstan to release water from the Toktogul Reservoir in exchange for electricity from Kazakhstan and Uzbekistan, smoothing seasonal variability, aligning incentives between upstream and downstream countries, and generating mutual benefits.

Modernization and infrastructure investment can improve aging systems and expand access. In the United States, the Infrastructure Investment and Jobs Act15 allocated $50 billion for water infrastructure upgrades. A significant portion of these funds has been disbursed, including for the removal of emerging contaminants and of lead pipes in order to improve access to clean drinking water. China’s South-North Water Diversion Project, one of the largest infrastructure investments in history, is redirecting billions of cubic meters of water from the water-rich south to the more arid north. Qatar, a water-poor state that has experienced rapid population growth in recent years, has mitigated challenges, such as contamination or the potential for depleted reserves, with a system of mega-reservoirs that are the largest of their kind in the world.

Technology can also enhance existing water infrastructure. In Singapore, South Korea, and Malta, water digitization networks and intelligent metering applications are cutting losses and reducing nonrevenue water. Cities like Barcelona have invested in sensor-based smart systems that monitor humidity, temperature, and atmospheric pressure to optimize water distribution and reduce usage. Smart irrigation systems, drip technologies, and AI-enabled soil and crop monitoring tools are proliferating globally, reducing water use while conserving yields.

Public-Private Models and Blended Finance

Governments can also help unlock private sector solutions. These solutions can help tackle challenges to water access, provide new approaches for large-scale capital mobilization, and boost efficiency.

Governments can deploy public capital to de-risk projects through guarantees, anchor investments, and cofinancing. Public-private partnerships have become a central vehicle for this approach, sharing risk and combining public balance sheets with private financing and operational expertise to accelerate deployment of both conventional infrastructure and AI-driven solutions. Targeted incentives, including grants, low-interest loans, and regulatory frameworks, can bring promising pilot programs to scale.

One class of approaches is blended finance, which brings private capital together with public or philanthropic capital to provide risk mitigation for private investors and facilitate project completion. Blended finance is a widely used approach that can help tackle market gaps and “crowd in” private sector investments. This can work across different infrastructure types, and it was the approach taken through the Climate Innovation and Development Fund,16 a collaboration across several project types spanning grid-scale energy storage, wind farms, and resilient aquaculture. One such water infrastructure example is DC Water’s Environmental Impact Bond,17 which was structured to isolate project performance risk and modernize stormwater runoff management in Washington, DC.

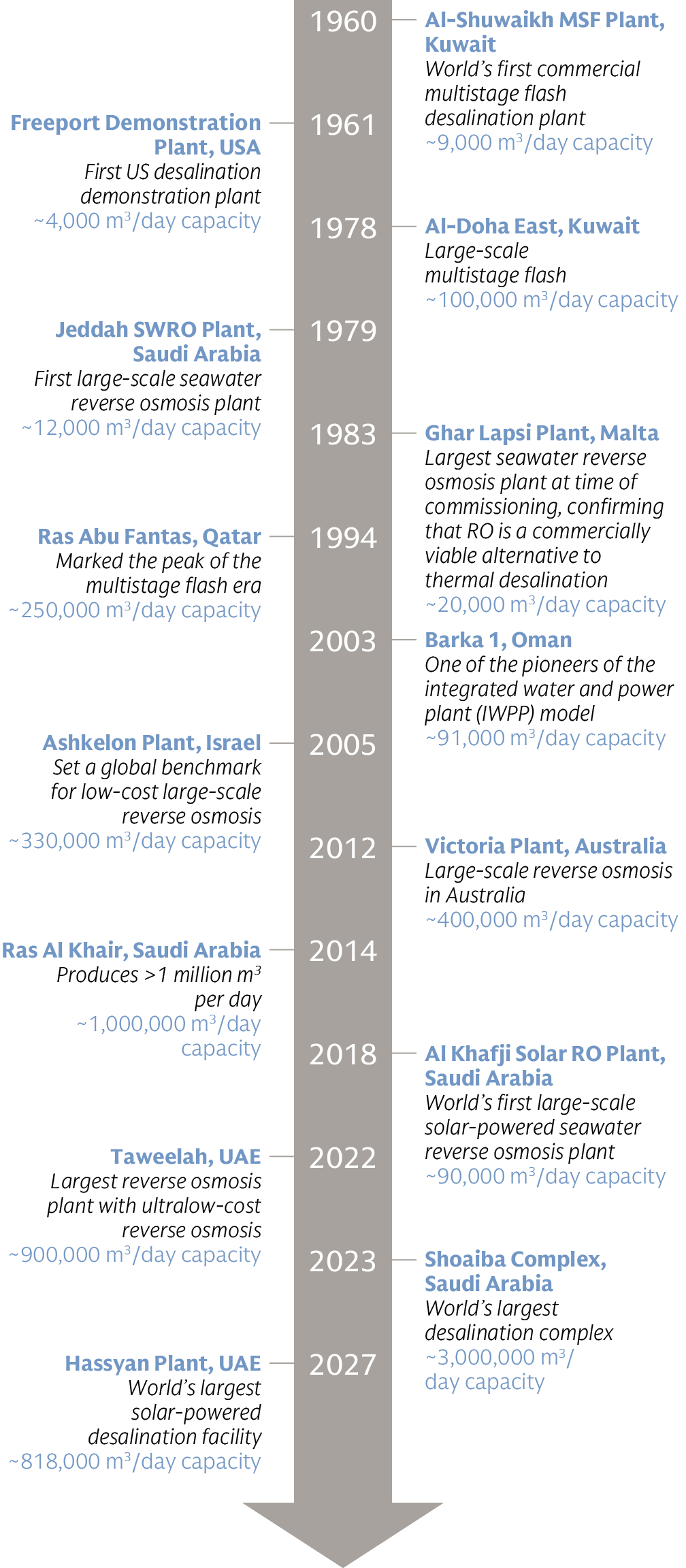

Government support can also catalyze private sector innovation and investment. Many of the world’s most freshwater-scarce countries nevertheless have ample access to salt water due to their long coastlines. Some are capitalizing on this geography by investing in desalination technologies and infrastructure. Gulf Arab nations are at the forefront of this trend, and between 70% and 90% of the drinking water in Saudi Arabia, Oman, and Kuwait comes from desalination plants. The UAE alone produces 14% of the world’s total desalinated water18 and is also piloting next-generation reverse-osmosis facilities powered by solar and other clean energy sources. Asian countries are investing as well. China’s water desalination market alone is projected to grow to $4.66 billion by 2033. The frontier for this sector is cost and energy reduction, with AI-optimized plant operations and renewable power integration as the primary levers.

Wastewater recycling offers a complementary supply-side solution that boosts the circularity of the water economy. Israel, itself a leader in desalination, recycles nearly 90% of treated wastewater for agriculture19 and now exports in excess of $2 billion worth of water technology annually to partners in the Arab Gulf, American Southwest, Latin America, and Australia. Singapore’s NEWater program, launched in 2002, converts used sewage water into ultraclean potable water via microfiltration, reverse osmosis, and ultraviolet disinfection, a more affordable process than desalination. This recycled water meets 40% of Singapore’s 440 million–gallon daily demand, with projections20 of meeting 55% by 2060. Such practices are expanding, and in the United States, California updated regulations in 2024 to allow sewage water to be treated and transformed into drinking water.

Market demands and government signals are providing strong incentives for the private sector to continue innovating. This innovation is creating novel solutions that draw on financial structures from outside of water and water infrastructure, including from power and other environmental markets and from other infrastructure sectors where novel de-risking and infrastructure approaches have been successful.

One approach is microfinance, including small loans, insurance, and other financial services extended to low-income populations. For water-related infrastructure, water.org takes an active approach. Through their WaterCredit solution, they catalyze capital (over $7.7 billion to date) to finance water and sanitation loans; their pay-it-forward model boasts loan repayment rates of 98%.

Private Sector Solutions and Financing Innovations

There have also been efforts to develop dedicated investment vehicles to channel capital to novel solutions. One example is the Sustainable Water Impact Fund.21 The fund’s focus includes water stewardship, and it aims to achieve both market returns and conservation goals through a close partnership between managers at RRG Capital Management and advisers at The Nature Conservancy. Investments aim to improve water efficiency and leverage novel design aspects, including performance-linked incentives and strategic asset targeting. The fund is also using sustainable forestry and conservation as strategic levers, such as by managing conserved land to improve water quality and creating basins to recharge groundwater reserves. More broadly, given the overlapping co-benefits between conservation and water resources, there are numerous opportunities to direct investment toward conservation actions that support water availability and quality. This is an approach with a long tradition, including prominent success stories like New York City’s water supply.

Particularly dependent on water and the largest global user, agriculture is an area of active focus for sustainable water use innovation. Because of the complexity of supply chains and of the interconnections between water resources and food systems, initiatives include both broad changes in incentives and investments in improved data and measurement of water. For large corporates, material improvements can stem from changed processes—such as assessment of water impacts, dependencies, and risks, as well as the establishment of context-dependent water-related targets. Major growers are also sponsoring initiatives aimed at smart irrigation approaches, which, given the scale of operation, can have meaningful impacts on local water stress.

As in other markets, tokenization is also emerging as a promising approach to challenges facing water markets. Tokenization can be used both to solve challenging water market issues—for example, by injecting liquidity and turning rights into traceable tokens that track water use across market participants and at different jurisdictional layers—and water infrastructure financing challenges. Tokenized financing can deliver credits for companies that conserve or recycle water through connections to flow meters. The UAE is testing a water-backed digital token22 that links verified physical water volumes to a tradable digital asset, with the aim of improving transparency and liquidity and connecting water more directly to capital markets. Because tokenization tends to be most effective in the context of liquid water rights and clear market structures, this innovation highlights the complementary relationship between market-oriented reforms and the deployment of innovative financing.

Conclusion

Water is at once the world’s most essential resource and one of its most poorly governed. The forces shaping the global water economy, including rising demand, changing weather patterns, chronic underinvestment in often aging and inadequate infrastructure, and the distorting effects of subsidies and outdated legal frameworks, are creating a challenge across borders and sectors.

However, there is a growing range of options to address these challenges. Market mechanisms are beginning to price water more effectively, private capital is increasingly flowing into water infrastructure, and technological innovation in areas such as desalination, wastewater recycling, and smart water management is attracting investment.

Addressing the global water challenge will require coordinated action across governments and private markets. Closing the investment gap will mean greater capital deployment but also governance reforms, including with regard to pricing, transparency, and water rights frameworks that allow supply to reach its highest-value uses. Geopolitical cooperation will be critical as transboundary water disputes and infrastructure vulnerabilities increasingly intersect with national security. The decisions made in the coming decade about how water is priced, financed, and managed are likely to drive market opportunities and shape economic resilience, social stability, and environmental sustainability.

Endnotes

1 Wondimu Musie and Girma Gonfa, “Fresh Water Resource, Scarcity, Water Salinity Challenges and Possible Remedies: A Review,” Heliyon 9, no. 8 (August 2023): e18685, https://doi.org/10.1016/j.heliyon.2023.e18685.

2 UNICEF Data, “Drinking Water,” last updated August 2025, accessed May 5, 2026, https://data.unicef.org/topic/water-and-sanitation/drinking-water/.

3 World Economic Forum, Bridging the €6.5 Trillion Water Infrastructure Gap: A Playbook, in collaboration with Acea and the University of Cambridge (Cologny/Geneva: World Economic Forum, December 2025), accessed May 5, 2026, https://reports.weforum.org/docs/WEF_Bridging_the_6.5_Trillion_Water_Infrastructure_Gap_A_Playbook_2025.pdf.

4 Yoon Young Chung, Federico Darakdjian, and Tom Leahy, “When AI Meets Water Scarcity: Data Centers in a Thirsty World,” MSCI, December 9, 2025, https://www.msci.com/research-and-insights/blog-post/when-ai-meets-water-scarcity-data-centers-in-a-thirsty-world.

5 Omer Karasapan, “Striving for Water and Food Security,” The Cairo Review of Global Affairs, Winter 2020, https://www.thecairoreview.com/essays/striving-for-water-and-food-security/.

6 James Wagner, Emiliano Rodríguez Mega, and Somini Sengupta, “Mexico City Has Long Thirsted for Water. The Crisis Is Worsening,” New York Times, May 18, 2024, https://www.nytimes.com/2024/05/18/world/americas/mexico-city-water.html.

7 International Trade Administration, “Jordan - Environment and Water Sector,” Jordan Country Commercial Guide, last published February 26, 2026, https://www.trade.gov/country-commercial-guides/jordan-environment-and-water-sector.

8 Edward Ring, “Water, Water Everywhere—Except in California’s Reservoirs,” Wall Street Journal, April 17, 2026, archived at Archive Today, accessed May 5, 2026, https://archive.is/xPwsj.

9 UN-Water, “UN World Water Development Report 2025,” March 21, 2025, https://www.unwater.org/publications/un-world-water-development-report-2025.

10 NASA/JPL-Caltech, “Map of Groundwater Storage Trends for Earth’s 37 Largest Aquifers,” GRACE-FO, accessed May 5, 2026, https://gracefo.jpl.nasa.gov/resources/48/map-of-groundwater-storage-trends-for-earths-37-largest-aquifers/.

11 Sarita Chaganti Singh, Shivam Patel, and Ariba Shahid, “India-Pakistan Water Treaty Remains Suspended despite Ceasefire, Sources Say,” Reuters, May 10, 2025, https://www.reuters.com/world/asia-pacific/india-pakistan-water-treaty-remains-suspended-despite-ceasefire-sources-say-2025-05-10/.

12 Australian Taxation Office, Register of Foreign Ownership of Water Entitlements: Report of Registrations as at 30 June 2023 (Canberra: Australian Government, 2024), accessed May 5, 2026, https://foreigninvestment.gov.au/sites/foreigninvestment.gov.au/files/2024-10/2023-rfo-water-entitlements.pdf.

13 Convention on the Law of the Non-Navigational Uses of International Watercourses, opened for signature May 21, 1997, 2999 U.N.T.S. 77, entered into force August 17, 2014, United Nations Treaty Collection, accessed May 5, 2026, https://treaties.un.org/Pages/ViewDetails.aspx?src=TREATY&mtdsg_no=XXVII-12&chapter=27&clang=_en.

14 Roberto Barragan, “For Water Conservation, Lawmakers Should Okay ‘Decoupling,’” Capitol Weekly, August 10, 2022, https://capitolweekly.net/for-water-conservation-lawmakers-should-okay-decoupling/.

15 U.S. Environmental Protection Agency, Bipartisan Infrastructure Law: State Revolving Funds Implementation Memorandum (fact sheet, March 2022), https://www.epa.gov/system/files/documents/2022-03/bil-srf-memo-fact-sheet-final.pdf.

16 Goldman Sachs, “Climate Innovation and Development Fund,” accessed May 5, 2026, https://www.goldmansachs.com/our-firm/sustainable-finance/cidf.

17 DC Water, “Environmental Impact Bond,” accessed May 5, 2026, https://www.dcwater.com/environmental-impact-bond.

18 Gulf News Report, “Abu Dhabi Produces 9% of World’s Total Desalinated Water, Official Says at MENA Forum 2022,” Gulf News, last updated March 15, 2022, https://gulfnews.com/uae/environment/abu-dhabi-produces-9-of-worlds-total-desalinated-water-official-says-at-mena-forum-2022-1.86461064.

19 U.S. Environmental Protection Agency, From Water Stressed to Water Secure: Lessons from Israel’s Water Reuse Approach: 2022 U.S. Delegation Summary (EPA-822-S-23-001, March 2023), https://www.epa.gov/system/files/documents/2023-03/From%20Water%20Stressed%20to%20Water%20Secure%20-%20Lessons%20from%20Israel%27s%20Water%20Reuse%20Approach.pdf.

20 PUB, Singapore’s National Water Agency, “PUB Pushes the Frontier of Water Technology to Reach Future Energy and Sludge Reduction Targets,” press release, July 4, 2018, https://www.nas.gov.sg/archivesonline/data/pdfdoc/20180704002/Press%20Release_PUB%20RD%20blueprint.pdf.

21 RRG Capital Management and NatureVest, Sustainable Water Impact Fund 2024 Impact Report (The Nature Conservancy), accessed May 5, 2026, https://www.nature.org/content/dam/tnc/nature/en/documents/s/u/Sustainable-Water-Impact-Fund-2024-Impact-Report.pdf.

22 Manoj Nair, “Dubai’s DMCC in Project to Launch World’s First Digital ‘Water’ Token,” Gulf News, last updated June 17, 2025, https://gulfnews.com/business/markets/dubais-dmcc-in-project-to-launch-worlds-first-digital-water-token-1.500166367.

Disclaimer

This document has been prepared by the Goldman Sachs Global Institute and the Sustainable Finance Group and is not a product of Goldman Sachs Global Investment Research. The opinions and views expressed herein are as of the date of publication, subject to change without notice, and may not necessarily reflect the institutional views of Goldman Sachs or its affiliates. Goldman Sachs does not undertake to update this document, or any other information contained in this document, to reflect potential changes or events. The material provided is intended for informational purposes only, and does not constitute investment, legal, or tax advice, a recommendation from any Goldman Sachs entity to take any particular action or be used as a basis for any other investment decision, or an offer or solicitation to purchase or sell any securities or financial products. Any forward-looking statements, case studies, computations or examples set forth herein are for illustrative purposes only. Past performance is not indicative of future results. Neither Goldman Sachs nor any of its affiliates make any representations or warranties, express or implied, as to the accuracy or completeness of the statements or information contained herein and disclaim any liability whatsoever for reliance on such information for any purpose. Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness, or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources. No reports, documents, or websites that are cited or referred to in this document shall be deemed to form part of this document. No representation or warranty is made by Goldman Sachs as to the quality, completeness, accuracy, fitness for a particular purpose, or non-infringement of information obtained from outside sources. Each name of a third-party organization mentioned is the property of the company to which it relates, is used here strictly for informational and identification purposes only and is not used to imply any sponsorship, affiliation, endorsement, ownership or license rights between any such company and Goldman Sachs. Should you click a hyperlink contained in this document directing you to an external third-party website that Goldman Sachs does not own or operate, you acknowledge and agree that Goldman Sachs is not responsible for the products, services, or content provided on that site and you must refer to that external website’s terms, privacy, and security policies for details. This material should not be copied, distributed, published, or reproduced in whole or in part or disclosed by any recipient to any other person without the express written consent of Goldman Sachs.

© 2026 Goldman Sachs. All rights reserved.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.