Energy

Why Oil Prices Could ‘Grind Lower’ amid the US-Iran Deal

Oil has declined since US President Trump announced an interim deal with Iran to extend a ceasefire and gradually reopen the Strait of Hormuz. In the near term, even as the flow of oil through the Strait may increase meaningfully, markets probably already reflect the agreement, says Jerome Dortmans, co-head of Global Oil and Products Trading in Goldman Sachs Global Banking & Markets.

Are oil prices likely to fall further?

“The bulk of the price movements are probably priced in,” says Dortmans, who is also head of Americas and EMEA Oil Products Trading. “This is by no means over, but we seem to be progressing toward a cooled-off environment that will allow the oil market to find a healthier balance in terms of price.”

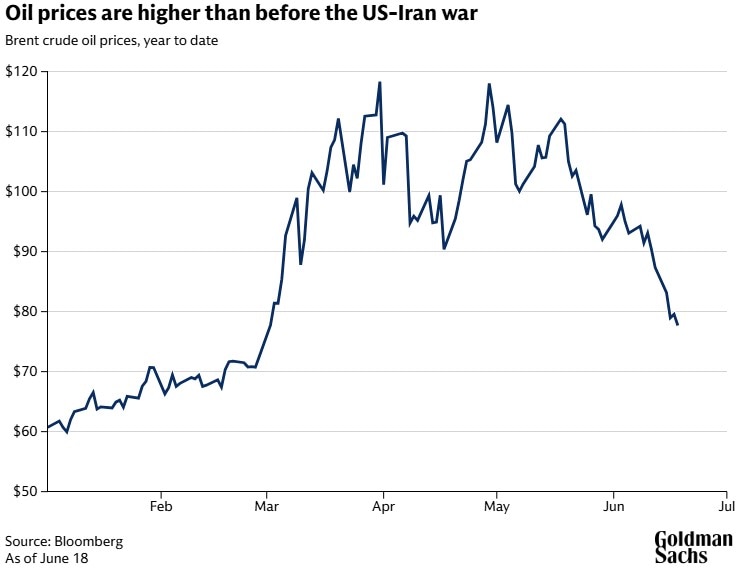

Benchmark Brent oil has fallen to about $76 per barrel (as of June 18), from a high of around $118 in April during the war between Iran and the US and Israel. Prices remain higher than they were before the conflict. Brent was trading at about $60 per barrel in early January.

Dortmans points out that the US and Iran have yet to reach a final settlement, and many technical details for a longer-term resolution are yet to be agreed on. At the same time, he says the oil market has likely entered a different paradigm. While energy prices are likely to gyrate along the way, oil may gradually decline. The market is likely to “grind lower,” Dortmans says, even as some news headlines could cause prices to jump temporarily.

Lower global stock levels as a result of the conflict will make lower prices critical in the coming months, Dortmans notes: Demand in the northern hemisphere for products such as gasoline and diesel, for example, will ramp up meaningfully in the third quarter.

How are companies and investors responding to recent oil price declines?

As oil prices fall, major oil consumers are once again becoming more active hedging forward oil prices, Dortmans says. Some institutional investors, meanwhile, are positioning for oil prices to fall to $50 or $60 per barrel “pretty quickly,” he says. “Their expectation is that this conflict will be resolved and the speed of building surpluses in crude will be significant,” he says. Dortmans cautions that such low oil prices could cause production gains made over the last few months to be reversed. The supply picture for high-cost producers could become more challenging.

Oil spiked when Iran closed the Strait of Hormuz, through which around 25% of the world’s seaborne oil transited before the war. However some oil had probably already begun to flow through the Strait following a ceasefire in April, Dortmans says, and those shipments are likely to accelerate. That flow is expected to come from vessels that have been unable to leave the Strait of Hormuz as well as from oil produced in Iran, he says.

The US and Iran signed an interim deal this week that extends a ceasefire for 60 days and allows Iran to export during that period. The oil market will likely trade in a more “normalized fashion” for the first half of that 60-day period, Dortmans says. But things could again become more complicated if there’s a perception within the market that the parties are not moving toward a more permanent peace agreement.

Why haven’t oil prices risen higher during the US-Iran conflict?

While oil supplies through the Strait of Hormuz have been greatly curtailed over the past few months, several key adjustments have taken place, Dortmans says. Refiners in Asia purchased oil at much higher prices after the Strait closed, which resulted in lower demand for their products. Some Middle East crude oil producers were able to reroute some oil flows from the Strait to pipelines. China reduced its demand for oil much more than many in the market expected, Dortmans says, and a number of countries also released oil from their strategic petroleum reserves (SPR).

High oil prices have also been an incentive for some producers outside the Middle East to ramp up their oil output. Production from Brazil, Kazakhstan, and Venezuela, for example, has increased.

Dortmans expects some of those factors that allowed the market to cope to fade, or even reverse, going forward, especially on the demand side. Global oil stocks have been greatly diminished and will need to be replenished, both commercial and strategic.

While there is potential for surpluses of oil to emerge toward the end of the year and into 2027, Dortmans says, he expects in this initial phase for Brent oil to trade around a floor of about $70-$75 per barrel.

Is the oil market at risk of a glut?

If the US and Iran reach a comprehensive peace deal reasonably soon, oil prices could enter a much more “benign” phase, Dortmans says. Iran could be in a position to export significantly more oil, for example. Much will also depend on how quickly oil producers in the region can ramp up production again, he says.

Some countries in Asia may look to increase their storage of oil to protect their economies from future energy disruptions, he says, and China’s demand will likely climb again eventually.

“Due to higher prices, the market has clearly run down global stock balances, not just in crude oil but across the entire oil complex including petrochemical feedstocks and end products,” Dortmans says. “We are going to go through a period of rebuilding those stocks if we see demand return to pre-conflict levels.”

Dortmans says oil investors should also be mindful of the war between Ukraine and Russia, which is a key oil producer and has had its refining capacity damaged during the war. In the near-term, news reports suggest that some western powers may seek to place further sanctions on Russian oil. However, should Ukraine and Russia reach a peace deal, more energy supplies from Russia could enter the market, Dortmans says.

In terms of the conflict between the US and Iran, Dortmans says traders and investors are largely of the mindset that the oil market will normalize. However, he notes that it is still important to guard against complacency, as the countries have yet to reach a peace agreement.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.