Retirement Reality Check: Insights From Companies and Their Employees

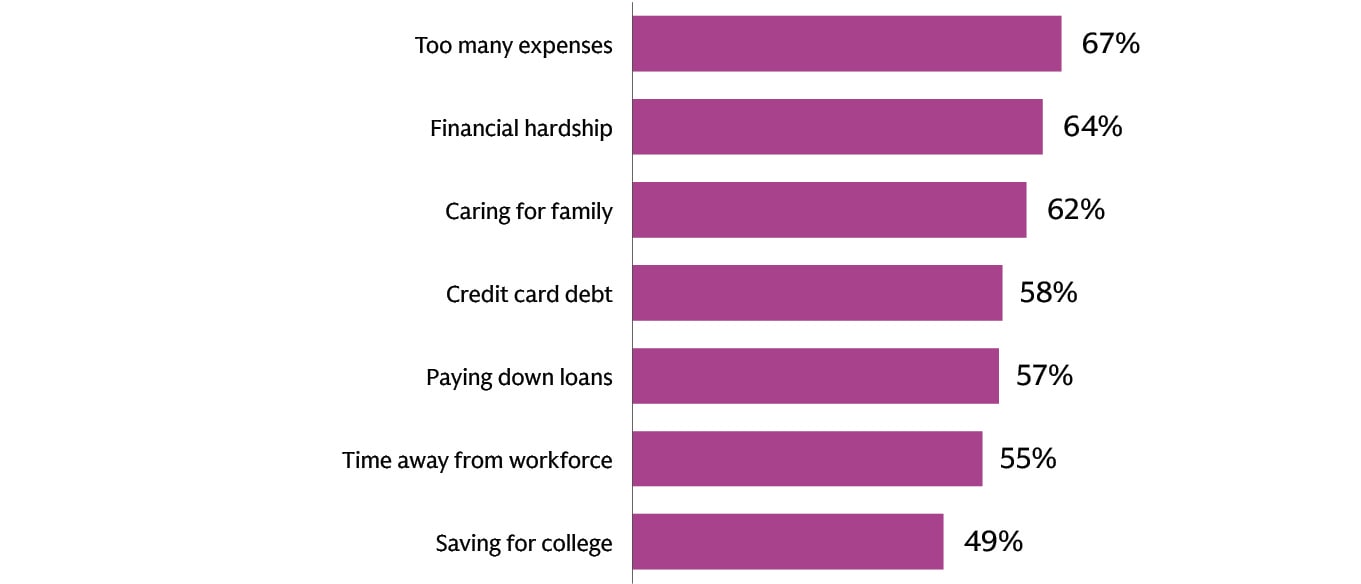

Over the past five years, Goldman Sachs Asset Management’s annual Retirement Survey & Insights Report has consistently surfaced a central theme: competing financial priorities are making retirement savings affordability harder for many individuals. As day-to-day demands rise—from debt repayment to caregiving, education expenses, and other household costs—savers often feel forced to make trade-offs that can disrupt long-term goals.

To better understand how human resource leaders are adapting to these and new challenges, Goldman Sachs Asset Management conducted an inaugural survey1 of 250 chief human resource officers at employers that offer 401(k) or 403(b) plans. The survey identified how they approach plan design and what retirement income features they may be considering to support a growing list of employee needs. Over 5,000 retired and working individuals were also surveyed for their insights.

Employers and employees diverge on what constitutes retirement readiness

A notable disparity seems to exist between employers’ and employees’ perceptions of what constitutes being ready for retirement. Companies estimate that a median of 33% of their employees are on track for retirement, with only approximately 40% of employers believing that more than half of their workforce is adequately prepared. This indicates a cautious outlook from the employer perspective.

In contrast, a significant majority of working respondents, 68%, report a more optimistic view of their own retirement preparedness, believing they are on or ahead of schedule for retirement. However, this optimism seems to be further contradicted because 58% of those same working respondents believe they will outlive their savings.

What this suggests: Confidence isn’t the same as readiness. The divergence may underscore the value of personalized planning assumptions and participant-specific guidance that can help employees calibrate expectations and take action earlier.

The bigger message: Traditional plan design alone may not resolve challenges rooted in affordability and other concerns—raising the stakes for employers to offer guidance and advice, personalization, and practical planning tools.

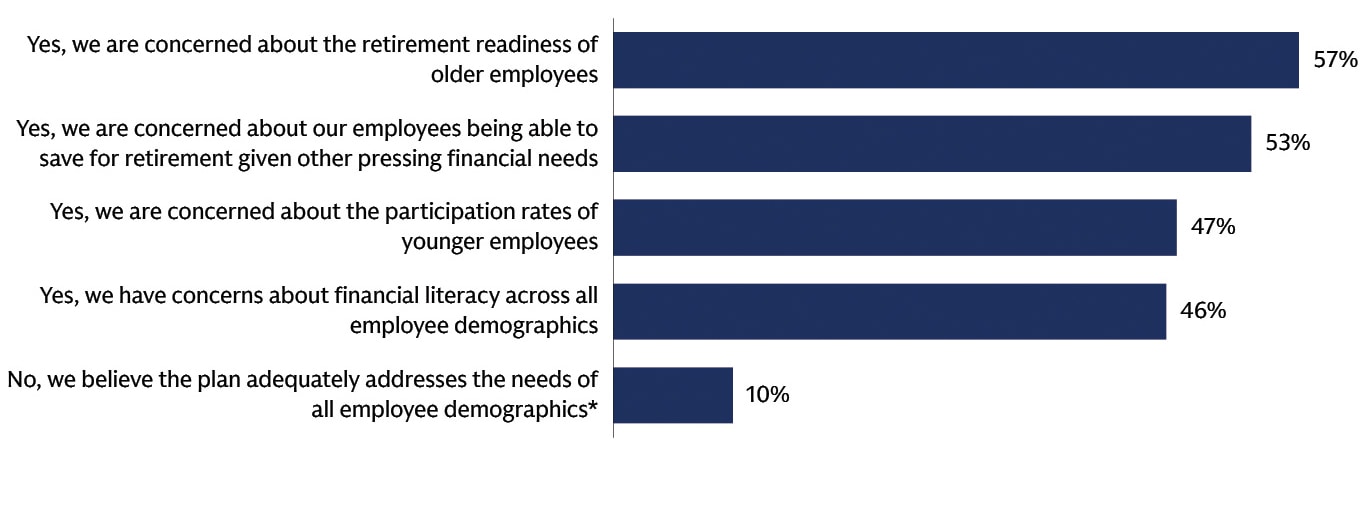

Employers and employees see real gaps in retirement preparedness

A number of employers surveyed believe there are unmet needs or demographic trends that require attention. Areas of concern reported include:

- Retirement readiness among older employees

- Retirement savings affordability given financial pressure

- Participation trends among younger employees

- Financial literacy needs

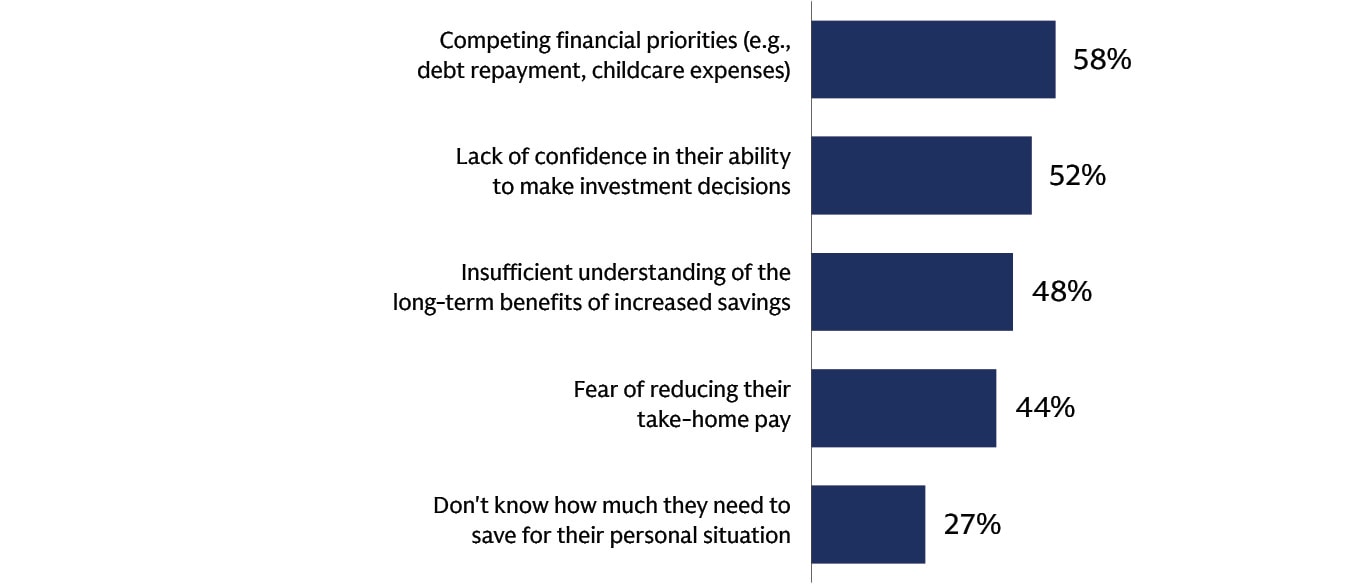

Employers pointed to several drivers behind insufficient saving, including competing financial priorities. Employees agreed—their competing priorities are detailed in the chart below.

Employers prioritize financial stability and retirement readiness amidst evolving challenges

Employers are increasingly explicit about why they are investing time and attention in benefits strategy: financial wellbeing impacts employees—and the business. The top priorities cited center on helping employees build stability and make better use of the benefits already available.

- 72% of respondents cited financial stability and retirement readiness as top priority.

- 41% of employers have adopted a holistic benefits philosophy that integrates retirement benefits into broader efforts to support employee health and financial wellness. This approach is focused on helping employees build stability and make better use of available benefits, in addition to strengthening personalized, goal-based retirement planning.

Why it matters: Personalized, goal-based retirement planning can be core for savers. The convergence of financial education, digital tools, and one-on-one advice is creating a continuous planning experience. AI is being integrated into retirement planning aiming to enhance participant engagement and provide tailored investment recommendations.

Investment menu innovation is accelerating—especially around personalization

Employers report they are evaluating several investment menu changes over the next 12 months, with emphasis on finding solutions that are more protective, tailored, and diversified. (Diversification does not protect an investor from market risk and does not ensure a profit.)

Common considerations include:

- Enhancing inflation protection options—strategies may include incorporating a broader range of asset classes

- Adding personalized investment solutions; strategies may include introducing or enhancing managed accounts

Another consideration is the integration of private market strategies. Bipartisan retirement legislation and new regulations are creating a supportive environment for innovation in retirement planning. The White House issued an Executive Order titled Democratizing Alternative Assets for 401(k) Investors, which aims to develop new regulations allowing employers to incorporate alternative asset classes, such as private market investments. This move is expected to provide greater flexibility to assess and potentially include these asset classes in their investment menus.

On what participants want, employers appear directionally aligned: personalized solutions rank as a top desired enhancement, alongside professionally managed portfolios that may offer higher long-term return potential (with possible higher risk).

Retirement income for life and remaining in the plan are top priorities—but barriers exist

Both employers and employees agree that guaranteed lifetime income is a top priority. Companies are increasingly focused on solutions that extend beyond accumulation into the retirement transition. Many actively encourage participants to keep assets in their retirement plan after termination or retirement, reflecting a growing emphasis on continuity and retention.

But employers also cite meaningful headwinds to offering guaranteed income solutions, including:

- Low participant engagement (41%)

- Difficulty understanding new offerings (36%)

Retirement income is rising on the agenda, but employers want solutions that can overcome complexity and engagement barriers—not just add features . Two possibilities are:

- Target date funds (TDFs) with embedded annuities and

- Annuity marketplaces.

Asset managers and insurance companies are collaborating to create target date strategies that not only adjust asset allocation over time but also include an embedded annuity contract. For example, some TDFs now feature a guaranteed minimum withdrawal benefit within the target date series, directing part of a participant's account balance into a guaranteed annuity. Alongside TDFs with embedded annuity features, annuity marketplaces are emerging as a key component of guaranteed income options. These marketplaces provide a platform for participants to explore and select annuity products that suit their retirement needs.

Advice and managed accounts are becoming foundational

In-plan advice is increasingly viewed as a necessary layer to support more sophisticated plan design. Many companies report that managed accounts are already available, with additional companies considering adoption.

This research highlights a clear shift: employers recognize the growing complexity of their employees’ financial lives and are increasingly exploring solutions that blend personalization, engagement, and innovation aiming to improve retirement outcomes.

For more detailed findings from Goldman Sachs Asset Management, read the Plan Sponsor Survey 2026: Working Together to Develop Solutions and Exploring the New Generation of Retirement.

Disclosures

1 Source: Goldman Sachs Asset Management’s Plan Sponsor Retirement Survey; Refer to the report for full disclosures. The survey was conducted by Goldman Sachs Asset Management and Escalent between June 27, 2025–July 21, 2025 Views expressed are those of survey respondents.

Advisory services offered by Goldman Sachs Wealth Services, L.P. (the “Adviser”), a registered investment adviser, affiliate of Goldman Sachs & Co. LLC ("GS&Co."), and a subsidiary of The Goldman Sachs Group, Inc., a worldwide, full-service investment banking, broker-dealer, asset management, and financial services organization. Goldman Sachs Ayco is a brand of Goldman Sachs Wealth Services, L.P. Brokerage services are offered through GS&Co. and Mercer Allied Company, L.P. (a limited purpose broker-dealer), both affiliates of the Adviser and members FINRA/SIPC.

THESE MATERIALS ARE PROVIDED SOLELY ON THE BASIS THAT THEY WILL NOT CONSTITUTE INVESTMENT ADVICE AND WILL NOT FORM A PRIMARY BASIS FOR ANY PERSON'S OR PLAN'S INVESTMENT DECISIONS, AND GOLDMAN SACHS IS NOT A FIDUCIARY WITH RESPECT TO ANY PERSON OR PLAN BY REASON OF PROVIDING THE MATERIAL OR CONTENT HEREIN. PLAN FIDUCIARIES SHOULD CONSIDER THEIR OWN CIRCUMSTANCES IN ASSESSING ANY POTENTIAL INVESTMENT COURSE OF ACTION.

This material is provided at your request for informational purposes only. It is not an offer or solicitation to buy or sell any securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities. This material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Individual portfolio management teams for Goldman Sachs Asset Management may have views and opinions and/or make investment decisions that, in certain instances, may not always be consistent with the views and opinions expressed herein.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

In the United States, this material is offered by and has been approved by Goldman Sachs Asset Management, L.P., which are registered investment advisers with the Securities and Exchange Commission.

Confidentiality

No part of this material may, without Goldman Sachs Asset Management’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

© 2026 Goldman Sachs. All rights reserved.

Date of first use: March 5, 2026. Compliance Code: 495669-OTU-2485279.

Subscribe to Briefings

Our weekly newsletter delivers the latest insights on economic forces shaping markets—from Goldman Sachs leaders, economists, and investors around the world.

You can unsubscribe at any time. For information about how your personal data will be used, visit Privacy Information and Resources.